Scenario planning for NZ to December 2021

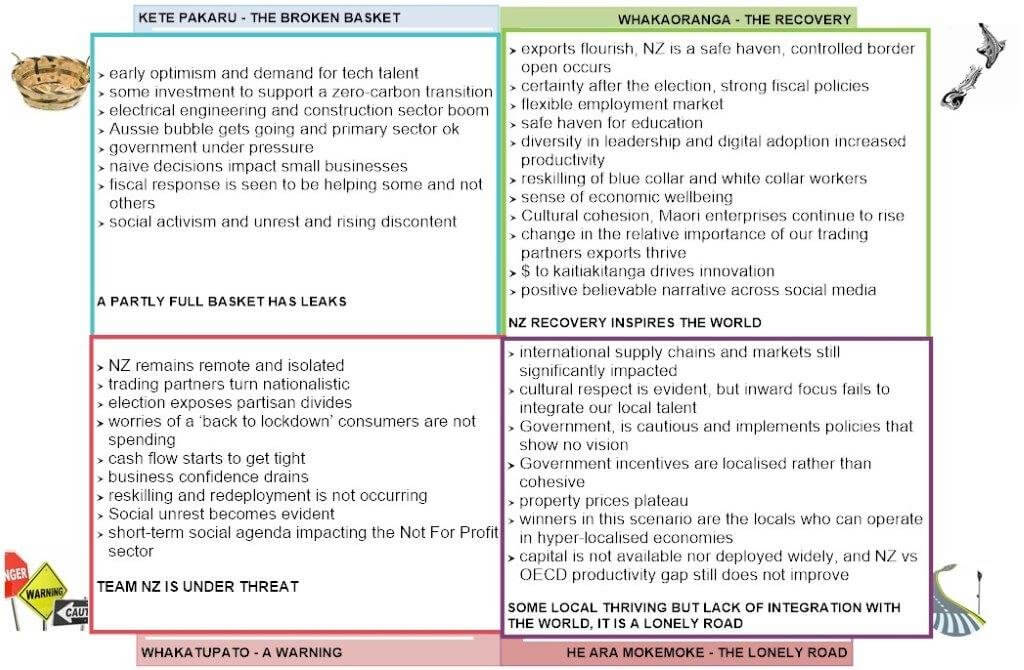

Whakatupato (the warning scenario)

Whakatupato (the warning scenario)

Our community and Team NZ is under threat.

The first of our plausible scenarios is a whakatupato (a warning). In Dec 2021 NZ remains remote and isolated as our borders remain restricted and free trade is impacted. Our major international trading partners turn nationalistic and protectionism affects our primary production exports. Locally a messy 2020 election exposes partisan divides with a potential hung parliament, which creates uncertainty for the business sector.

There is more and more disagreement about how Team NZ can be fixed, and positions become more entrenched. The impacts of multiple resurgences of COVID-19 in a vulnerable anxious nation are huge. There are continuous worries of a ‘back to lockdown’ play on the sentiment of consumers, who are not spending. General access to capital becomes very difficult and cash flow starts to get tight across the system, this leads to increased business failures and further discontent. Quantitative easing has only a limited impact. As business confidence drains, the general appetite for businesses to invest in reskilling wanes, and as unemployment rises it becomes evident that reskilling and redeployment of those who have lost their jobs, is not occurring.

This leads to a simultaneous reduction in investment into innovation, and businesses and consumers together become more and more risk-averse. Social unrest becomes evident especially as social mixing and events continue to isolate people and communities. Crime rates are rising, and a short-term social agenda dominates, impacting the Not For Profit sector’s longer-term community programmes. The accompanying negative partisan narrative across social media and from mainstream media further encourages the negative spiral.

Kete pakaru (the broken basket scenario)

Kete pakaru (the broken basket scenario)

Our NZ basket partly fills but is loose, badly made and has leaks

Under this second scenario, we see a surge in early optimism. Also, a rise in demand for tech talent so startups start to gain some momentum. There is an early impact of the buy-local movement and increasing government support to environmental-related activity. The energy sector is still quite active with some investment to support a zero-carbon transition. Primary industry connects to its markets, so the rural community is maintaining its position. Electrical engineering and some parts of the construction sector boom. Hitech and IT receive a boost from investment. We also begin to benefit from an Australasian bubble and certain sectors of the tourism industry start to revive.

However, after the election, the honeymoon is soon over and a government under pressure takes naive decisions that impact the ability of small businesses to transition to a green, circular economy. Oil and Gas support sectors, farming, fishing, logging plus downstream activities struggle under the burden. The SME community begins to question the sustainability of the environmental agenda. At the same time, the New Zealand government fiscal response is seen to be helping some and not others. This especially as the reality of not being able to easily reskill hits some people hard.

Consumers are starting to shift towards being more risk-averse and are generally more financially cautious and we’re starting to see a rise in social activism and unrest and rising discontent. As time passes, the difference in the impact of COVID-19 had on different economic classes becomes clearer. The unemployed and lower-paid hit with the double impact of higher exposure to the virus and the inability to convert to work-from-home. This contrasts with those who can work from home being seen to benefit from the comfort and safety of home and continued employment. Crime increases in pockets and any recovery is perceived to benefit some and not others, activism and unrest are on the rise.

He ara mokemoke (The lonely road scenario)

He ara mokemoke (The lonely road scenario)

We are moving forward, and some local thriving is evident, but for exports, productivity, and interconnectedness, it feels like a lonely road

Our third scenario suggests a team NZ that keeps things together, despite our international supply chains and markets still being significantly impacted for a good part of 2021. This scenario also considers the impacts of us not bringing Covid-19 under control. Severe border restrictions stay in place for some time to come. Importantly cultural respect is evident, but inward focus fails to integrate our local talent and ideas into a connected world, and there is a fine line between social cohesion and divergence.

There is also a reluctance for business to embrace change and introduce new thinking at a strategic level, short-termism with an inward focus becomes evident. The party that wins the election and comes to power as the Government, is cautious and implements policies that show no vision. There is a poor track record of execution and some legislative deficiency. There is a rising influence of NGOs which results in quite strong social leaning policies.

Tech innovation is local. Capital is not available nor deployed widely. The NZ vs OECD productivity gap still does not improve. New Zealand feels it can continue to go it alone, but we face skill shortages particularly IT capability and this impacts investment. Government incentives are localised rather than cohesive. Locally we are more inclined to spend as we are shielded from the worst of the pandemic. However, property prices plateau or start to decline without growth in immigration or investment.

The winners in this scenario are the locals who can operate in hyper-localised economies. They have very short supply chains and do not rely on goods imported from international markets, or other regions. They do not employ many people but provide essential services – food, health and social comforts. NZ doubles down on Localisation, rather than Globalisation – and some small, diverse towns regain relevance as places to live and grow. The pull of the cities is decreased. Self-sufficiency is a bigger driver of decisions. The basics are supplied at a local level and people travel to enjoy and experience regional specialities. You know the name of the butcher and know where your fruit grows. You band together as a community. Not because you want to, but because you must. And it turns out to be better than you expect.

Whakaoranga (the recovery scenario)

Whakaoranga (the recovery scenario)

NZ recovery inspires the world

Our Whakaoranga, or ‘recovery’ scenario, demonstrates that a positive vibrant outlook is also highly plausible. Primary market prices hold and exports flourish. NZ is a safe haven, so a controlled border open occurs. The positive perception of New Zealand enables a selective immigration policy. Purposefully combining key talent and businesses further enhances this upward spiral. There is a good deal of certainty after the election. A strong government with a robust and plausible plan is elected. It chooses to implement strong fiscal policies. Because there is a more flexible employment market, it allows the business sector to be more productive.

New Zealand’s relative COVID-19-free environment makes it an investment haven, particularly for professional services and high tech. As borders are opened to some medium/long term international visitors, NZ is seen as a safe haven for education. Education and long-term workers can begin returning, with the appropriate measures in place. We are seeing high levels of investment into innovation thanks to a supportive environment. The simultaneous investment by firms into a diversity of thought in their leadership and governance structures takes advantage of this trend. With no restrictive legislation, widespread digital adoption results in increased productivity and wealth generation.

There is evidence of blue-collar and white-collar workers successfully reskilling. In particular, 40+-year-olds who were displaced by COVID-19 shutdowns. Business embraces flexible worker trends, as well as new ways of working. It accommodates remote work and social distancing in a way that allows it to remain productive. A general sense of economic wellbeing allows a wider range of businesses to thrive. This includes those that might otherwise have struggled to survive the immediate impact of the pandemic.

Cultural cohesion and diversity are evident. Maori enterprises continue to rise and new entrants from outside NZ bring in ideas and capital. The Aussie and Pacific bubble works and “Go-local” boosts hospitality. This gains from the initial global travel bans and then puts the industry in a good position when travel resumes. We see a change in the relative importance of our trading partners. NZ gains direct access with one-on-one deals with several key trading partners. Finally, some smart Government intervention via fiscal support around kaitiakitanga drives innovation and investment into our circular economy, (recycling, primary and Hitech manufacturing and services). The rise of a discerning consumer internationally benefits New Zealand’s exports. Social media, and the media in general, support this with a positive believable narrative.

The flags

To get utility from this work, we have identified 12 flags (you may see others) that we feel should be monitored at least every month. The flags are indicators to which scenario we feel we are seeing at any moment over the next 18 months.